Budgeting: How to Buy a House in Toronto?

Budgeting: How to Buy a House in Toronto?

It’s a cliche in Canada to point out the cost of living crisis - but what’s surprising is that we are the G7’s most indebted country as well. Canadian household debt currently stands at about 110% of GDP.

That is to say we the Canadians, collectively (not any government) owe 10% more money to someone else (banks..) than all the value we produce in a year.

According to the CMHC about 75% of that debt come from mortgages. In order to gain some financial freedom your first priority after getting a mortgage is figure out how to get rid of it as fast as possible.

This post concerns itself with mortgages but the applies just as easily to any other saving priority.

The first step is figuring out how much house you can afford.

It’s tempting to start from a place of:

“This is how much house I want, what do I have to do to get it?”

But in a country where the two biggest economic centres have housing prices averaging over $1.1 Million as of May 2023, you need to make a realistic assessment of your current and future earnings potential.

Taking: the average Toronto home price of $1.15 Million, the average interest rate of 5.59%, the average payment schedule of every two weeks, and the average term of 25 years, and the average down payment of 25%. The family wanting an average house will need $4,896 a month after taxes just to cover their mortgage payments, and $6,635 when other standard operating costs such as water, power, internet, property tax etc. are factored in.

That means you need $79,620 after taxes just to cover the costs of paying for the house and its regular expenses.

A common (and rather absurd) trope in financial planning is that you should reserve 30% of your pre-tax income for housing. That multiplies to a pre-tax household income of about $239,000. If tears just formed in your eyes as well check out the article below for some happier math.

The second step is to think about the down payment.

Assuming you’ve decided to stick with a Toronto house, now you need to get saving (and investing preferably!). To get your hands on our example average house in the first place you will need a down payment of $287,500.

I’m going to make the assumption that two people save for the down payment together starting at age 25 to use at age 35 (ignoring inflation for now). That means each person is responsible for $143,750 over that 10 year period.

How Do I Get My Hands on $143,750 Without Dying From Excess Hustle?

There are two ways.

First, start a business (or multiple) and work on them. Using clever tactics you can get a lot more than you need quickly but we’ll save it for another post.

Second, diligent saving and medium term investing. Over the medium term you are looking for a steady return but also to limit your risk because there is a defined point at which you need the money in the future.

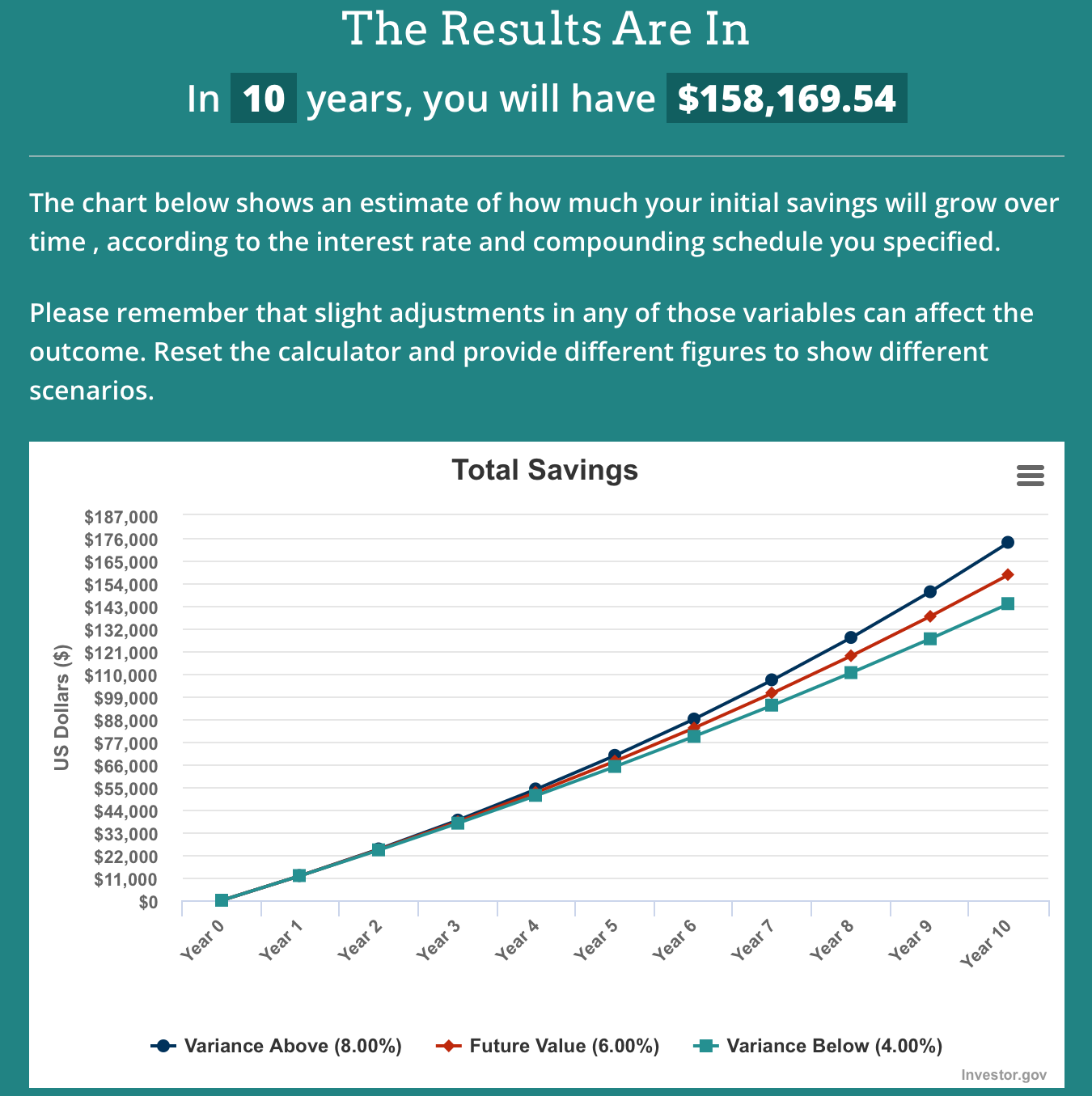

Refer to the following chart.

This assumes a Compounding Annual Return of 6% per year over a 10 year period when investing $1000 a month. This can be achieved using conservative dividend stocks of which this is a pretty good list.

Given that $12,000 after taxes is a lot in your mid 20s you can alternatively invest a smaller amount every month, increase the dividend yield (and therefore the risk of a price decline).

There are also taxes. Whenever you invest in the market (TFSA aside) you pay Capital Gains tax when you sell and take profit and Income Tax when you collect dividends.

The problem of taxes can be avoided entirely (legally) by contributing the maximum ($6,500) to your TFSA and making trades with it, contributing the remainder to your RRSP. You can make trades in a self directed RRSP the same way you can with a TFSA. For the purposes of a down payment on a home they will let you take a loan from your RRSP tax free as long as you pay it back within 15 years (after which they tax it like income).

Saving for a house in Toronto, or anywhere in Canada for that matter, is very hard - that’s why I dedicated an article about how not to do so. It is possible however with the right degree of farsighted financial planning, medium term sacrifice, and long term realism about the cost-benefit analysis of ownership.

That’s it for this week!

Sincerely,

James R. Davies.