How to Make Random Accidents Irrelevant..

And other things demonstrating the importance of insurance.

Life happens.

In the course of life, things happen. Much of that is in our control; some of it is not. Some things that are outside of our full control can cause huge problems for us and our families at any time.

What if there was a way to make those problems mostly irrelevant? A way to go through our day safe in the knowledge that the randomness of life needs to have few consequences beyond the shock of circumstance.

If it sounds like I’m trying to sell you insurance, I am. Not on a policy, but on the idea.

I’ve heard of this “Insurance”. But it Sounds Like it’s Only for Older People.

Wait a minute. Take a minute to understand the concept. Insurance is simply a financial product that transfers the risk of you or someone else losing something really important when they aren’t prepared for it.

Anyone who owns anything probably has something they might lose and can’t afford to replace at a moment’s notice. Insurance is for those people.

What Kinds of Insurance are There?

Almost everything of value in the world can be insured. Life insurance is the most obvious example, but you can also insure yourself against losing your house, your car, your jet, or even your $40 billion building. Most people, as they move through different stages of life, accumulate multiple overlapping policies to protect their most valuable assets.

Okay Sure But I’m Young - I Don’t See How Any of This Applies to Me…

Understandable.

Let’s take a hypothetical person, Dan, at different stages of his life.

Dan at 20:

Dan is 20 years old and still lives with his parents. He is going to trade school for pipe fitting because he heard the money working in oil and gas is good. He doesn’t drive because he lives in Toronto and knows that’s a very bad idea. He goes to the gym twice a week, eats a good diet, drinks moderately, and doesn’t have any risky hobbies. Dan also doesn’t think he needs insurance because his parents didn’t get it until they were like… 40?

Dan at 28:

Fast forward 15 years. Dan has been working in the oil patch for about 5 years now. To fit in with the people in his community, he’s picked up a cigarette smoking habit and now confidently goes through half a pack daily. He has had close calls at work (oil is slippery, and wells are dangerous places). He heard at one point that life insurance gets more expensive as you get older and is starting to think that it would be good to get some. He is about to get married to this nice girl in town, after all. He doesn't have kids yet, so he promptly forgets these thoughts and goes off to a night of hard drinking with the gang at the Patch Cantina.

Dan at 40:

The last 11 years have not been the kindest to Dan. He’s happily married and has two young kids he adores. The problem is that Dan’s doctors have told him that his hard drinking and cigarettes have left him with diminished heart and lung capacities that will actively get in the way of him being able to do manual labour. Luckily, Dan is up for a promotion to a desk job at the oil company he works for. He’s worried he may not get it, though, given that he’s had a few concussions from work-related injuries. He finally decides to get some life insurance.

The first advisor Dan talks to gives him a quote for the amount he wants, but:

“The price is awful!”, Dan says.

"Well, Dan, you’ve smoked for over ten years, work in a dangerous place, and have brain trauma... That means the risk to the insurance company of having to pay out your claim in any given year is higher than our average."

"This is B.S.!" cries Dan.

Dan marches over to his group benefits (company sponsored insurance) representative and demands a better rate, which he gets. The group admin warns Dan that if he gets laid off, his insurance goes with his job. He takes the plan anyway.

Enough with the storytelling!

Fine. But, in fairness, I actually met Dan; he was one of my clients. At age 55, he lost his job and his life insurance, and I had to sell him a smaller policy than he needed because he couldn't afford the rates for his age and health classification given the size of the policy.

So You’re telling me the Price of Insurance Goes Up Over Time?

Life Insurance, 100%. I won't go into too much detail about Life today; that needs a minimum of 3x separate posts. Safe to say for now that for every 1 unit increase in the risk of paying out policy money in a given year, the insurance company charges you more for the policy. Yes, this means that a 55-year-old male with a heart condition pays more for Health or Life Insurance than a 24-year-old female in the prime of health.

It also means that since your car is much more likely to get stolen in Alberta than in Ontario, Albertans pay high rates for their Car Insurance.

Additionally, residents of Miami pay far higher rates for home insurance (if they can get it at all) than people living in Toronto because in a given year, their house is far more likely to be destroyed.

Every single thing that increases or decreases the risk of an insurance payout necessarily affects the price you pay for it.

So are You Telling Me to Rush Out and Buy Life Insurance Now?

No, being in a rush is dangerous and leads to bad decision-making.

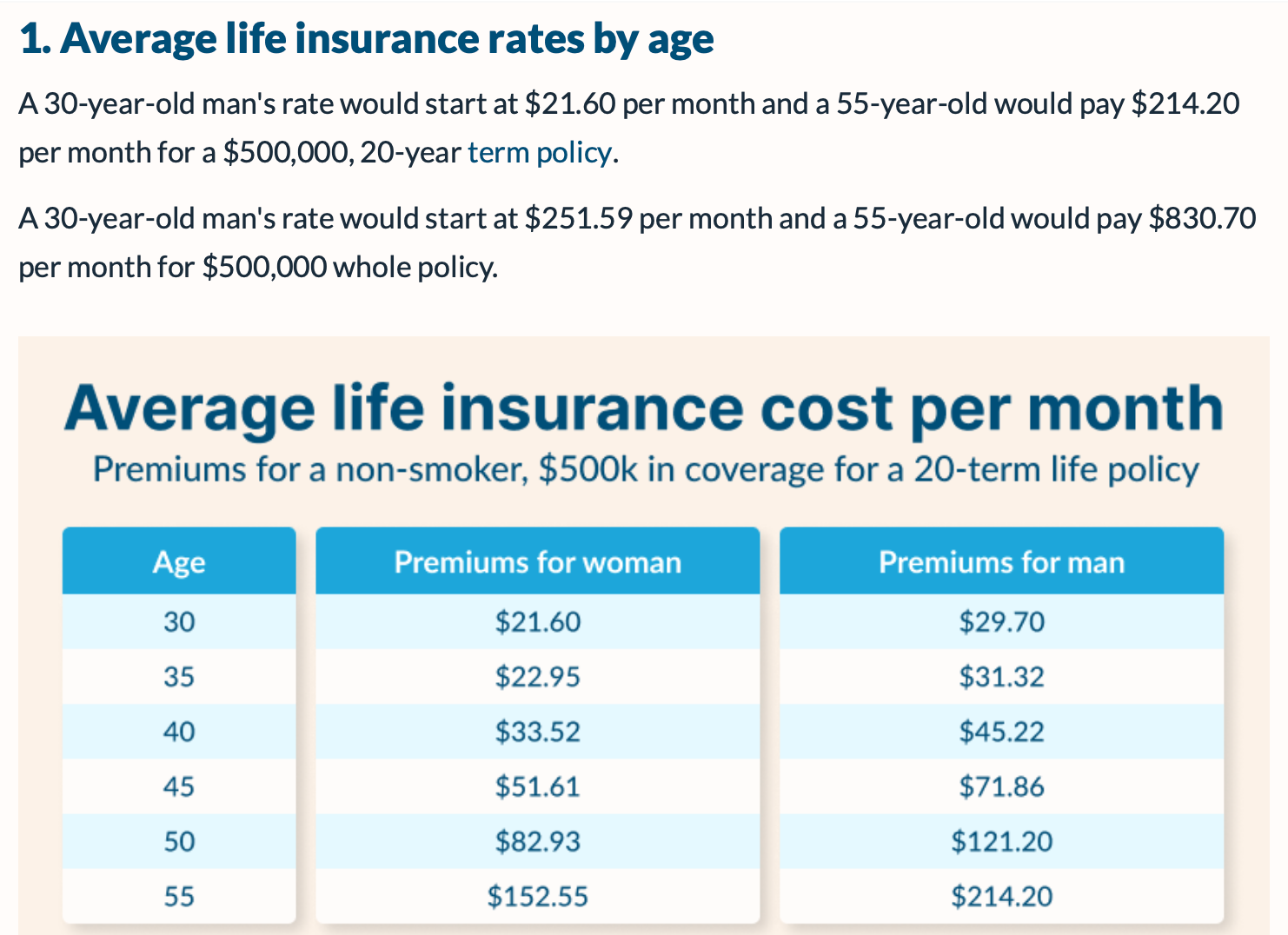

My goal is just to introduce you to the basics of insurance and explain how it can change in price over time depending on your life circumstances. That being said, I mentioned at the beginning that stuff happens. Insurance (any kind) is WAY cheaper before stuff happens than after. Please see the following chart.

And these are just the base rates for people who don't smoke cigarettes! Imagine if you've been seriously injured by 55; the rate increases are basically endless.

I will do a full article on the small details of Life Insurance as it is a critical topic that everyone should get to grips with ASAP.

For now, I hope this primer on the insurance industry has been valuable. I specifically chose not to provide any background on the business because it is long, complicated, and not productive in this case.

If you haven't already done so, I encourage you to check out the previous edition featuring Government Registered Savings Accounts as these are another critical component of building a stable financial future in the long term.

Until Wednesday,

James R. Davies